Case Study: Am I on the right track to retire at 55?

As a Reddit user posted:

nnnnnnnnnl've had a goal of retiring early since I saw my dad start enjoying retirement at 55. Just want to make sure I'm on the right track with my savings and investments to be able to do something similar.

n

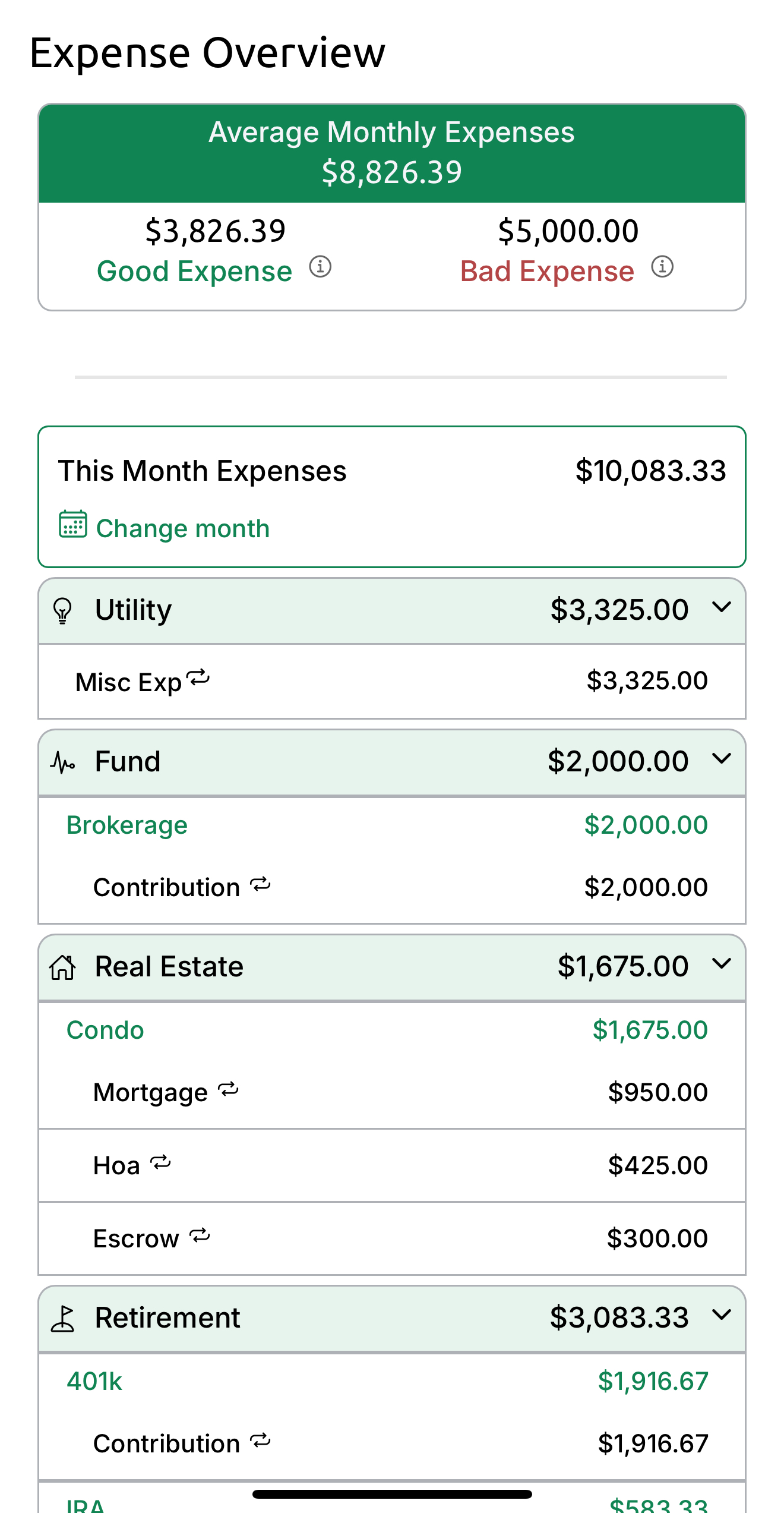

Me: 41, single, no kids. Currently, earn $175k in a management role. Right now, my yearly expenses are about $110k/year. Current net worth details:

nnnn- n

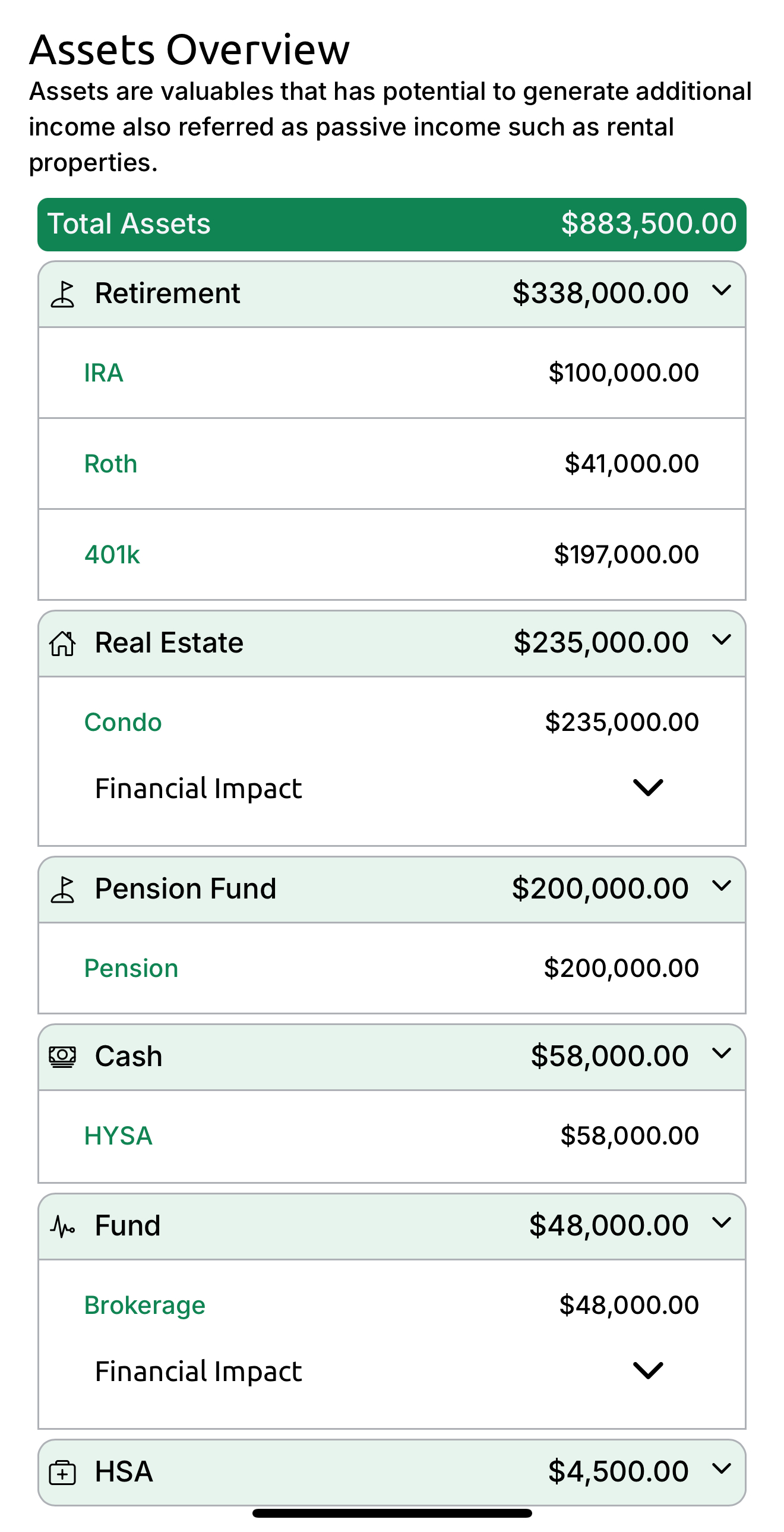

- Home: condo, ~$235k value, $169k mortgage balance at 3.25% nnnn

- 401k: $197k, invested in 2040 target date funds. Maxing out 401K nnnn

- Traditional IRA: $100k, invested in a 2040 and 2045 target date fund nnnn

- Roth IRA: $41k, invested in a mix of index funds and total market funds nnnn

- HSA: $4500, invested in FXAIX and maxing out. nnnn

- Brokerage: $48k, invested in total market funds. Putting $2K every month into it. nnnn

- Emergency Funds (HYSA): $58k n

My company has a pension plan, so I plan on working here at least 10 years so I can "retire" and claim it about $2k/month as an annuity.

nnnnHow to answer such questions?

nnnnFor anyone seeking F.I.R.E., estimating a financial portfolio is not easy. We consider estimating F.I.R.E. from two different angles.

nnnn- n

- Ability to meet expenses with enough passive income alone. nnnn

- Ability to meet expenses by liquidating the majority of the high-risk assets and reinvesting those in a low-risk option such as HYSA. n

Although option 1 is the best-case scenario and leads to infinite wealth, it is much more feasible for most people to achieve F.I.R.E. through option 2. Let's see how to analyze this financial profile and see future projections:

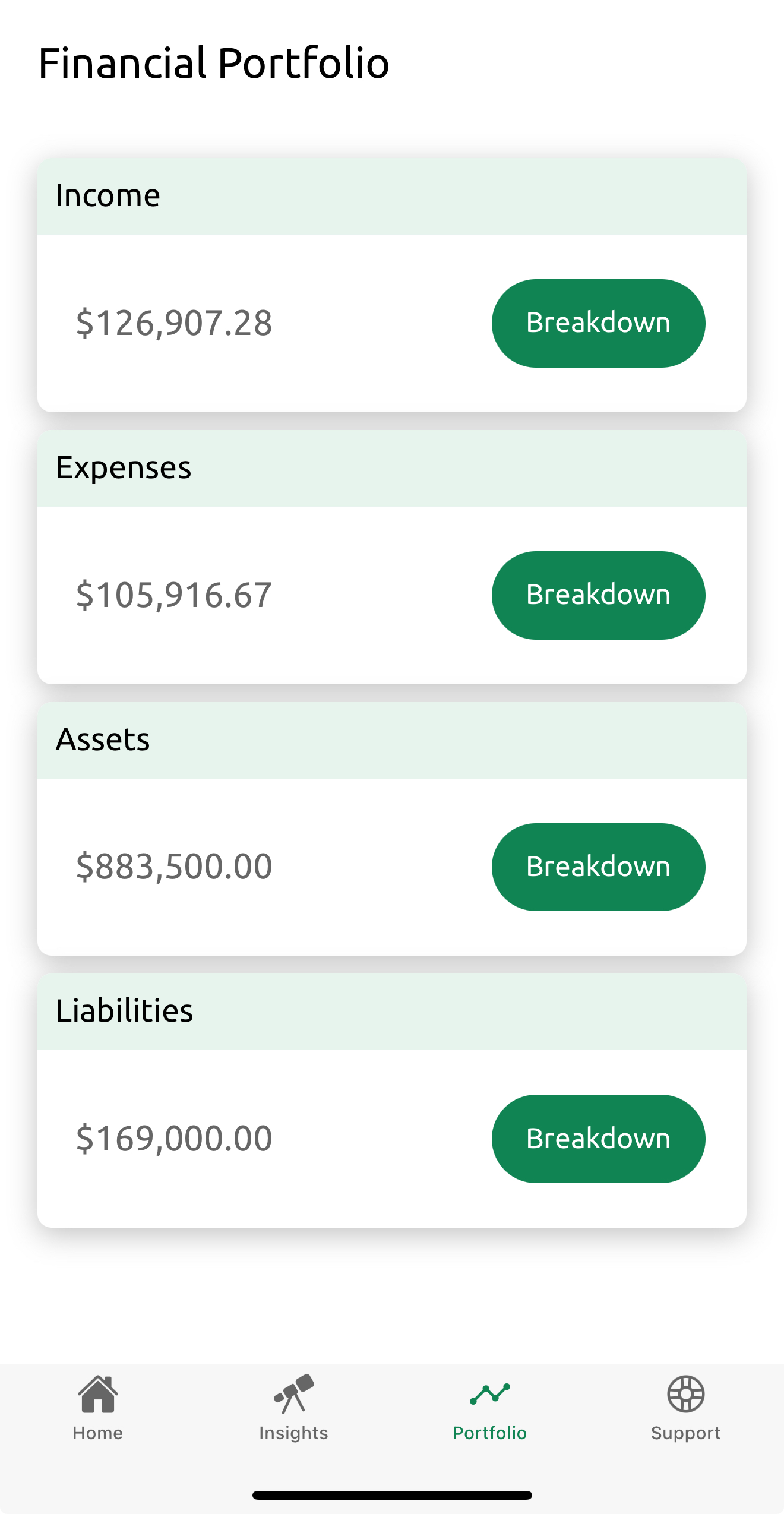

nnnnData Entry

nnnnEntering data is a relatively simple process for this type of analysis, as it only requires current values for different assets and overall contributions. This is how the entered data looks like:

nnnn

Analysis

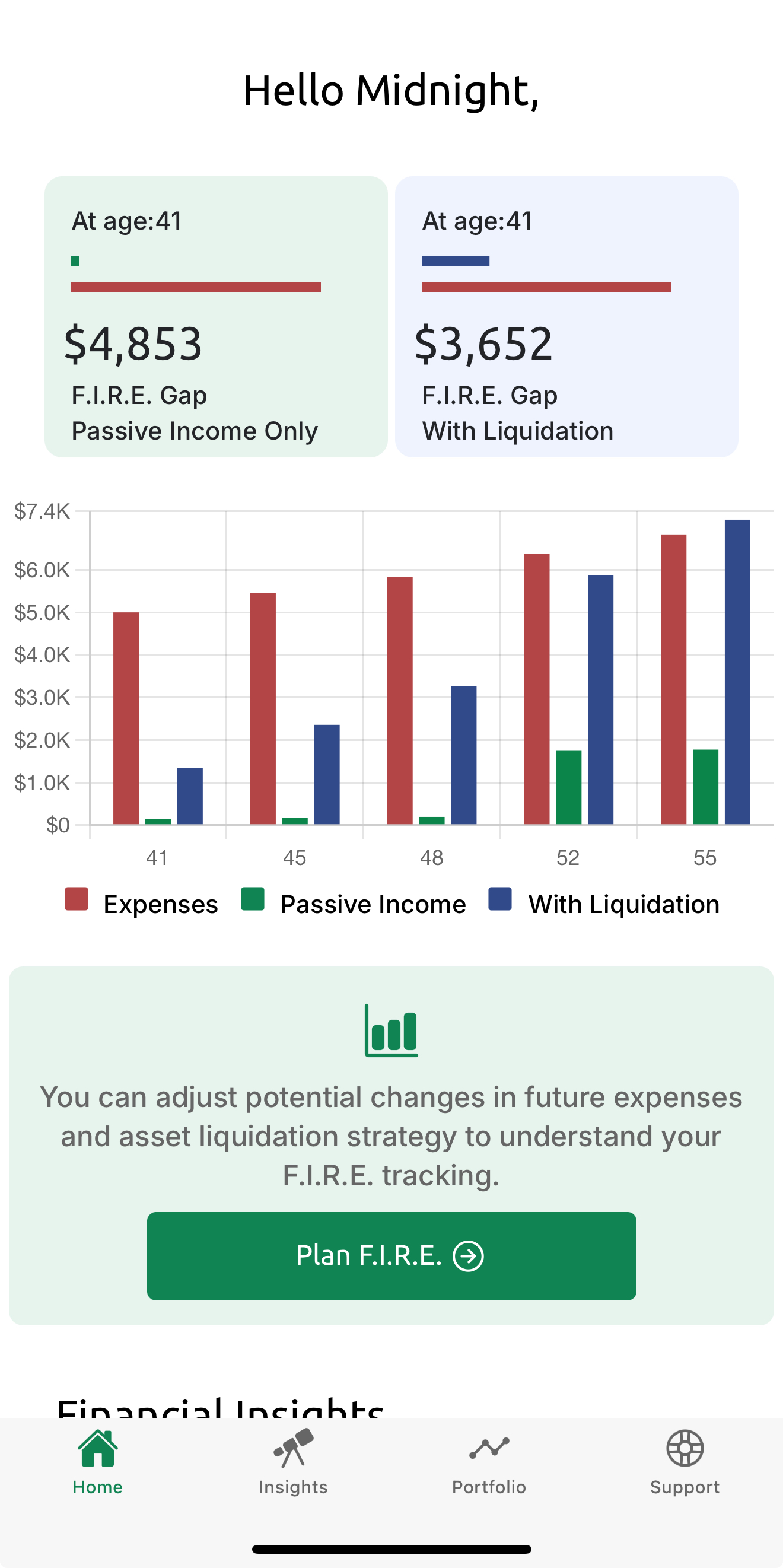

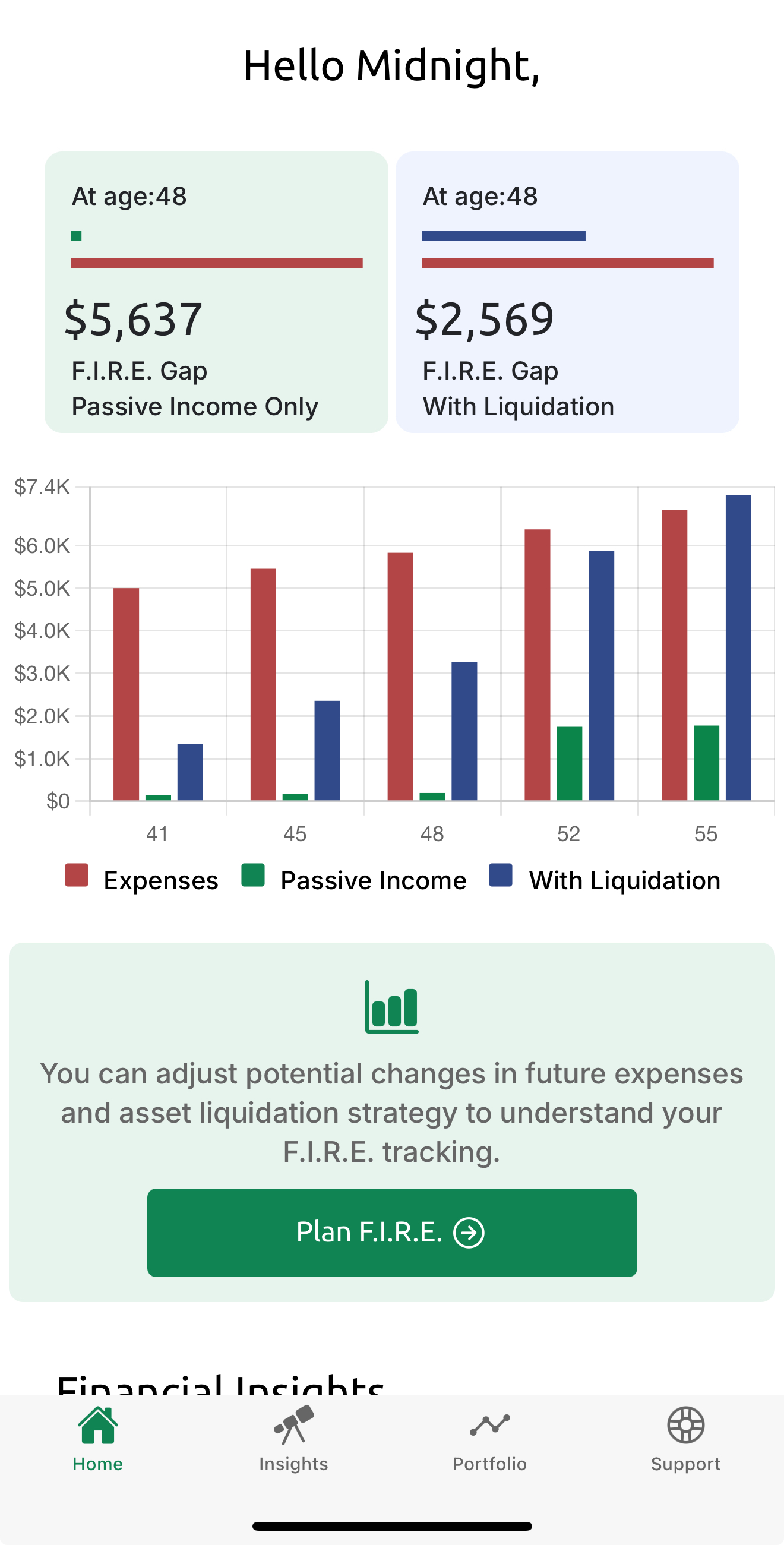

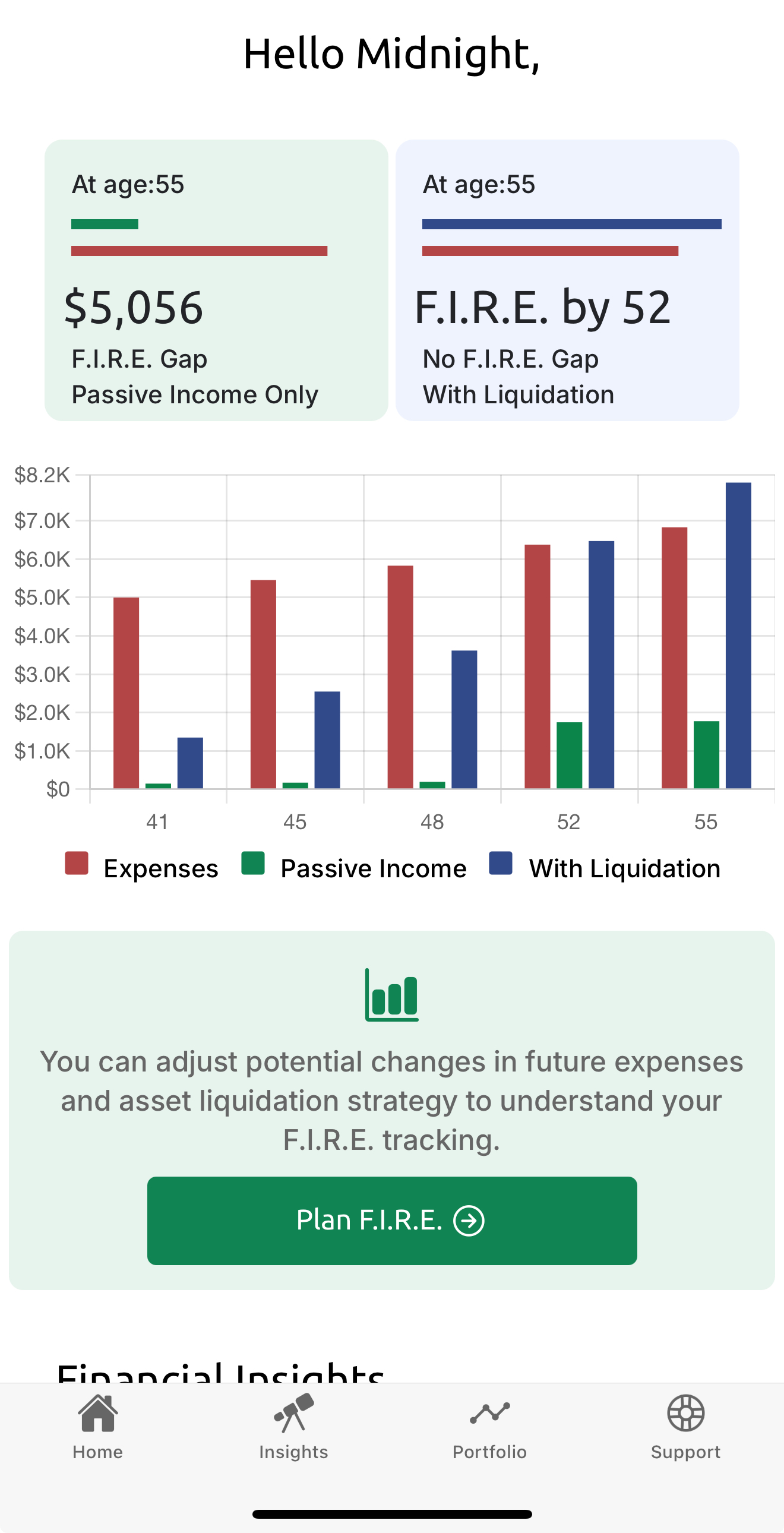

nnnnOnce the data is entered, the magic begins. The very first thing you will notice is a comparison chart of your expenses, passive income, and income by asset liquidation at regular intervals until your desired F.I.R.E. age. This is how it appears for this use case:

nnnn

What you see above is the top area showing three different snapshots of the F.I.R.E. gap at the current age of 41, at age 48, and at the target age of 55. The green box shows the gap with just passive income, whereas the blue box shows the gap with asset liquidation and reinvesting the money into a low-risk, low-return option. The above snapshots are visible by tapping on the bar chart on the age marker.

nnnnnnnnnAt a glance, it is evident that there will be a gap of $5,056 if only passive income is considered at the age of 55. However, F.I.R.E. can be achieved with asset liquidation by age 52, provided that asset liquidation is considered.

n

Deeper Dive

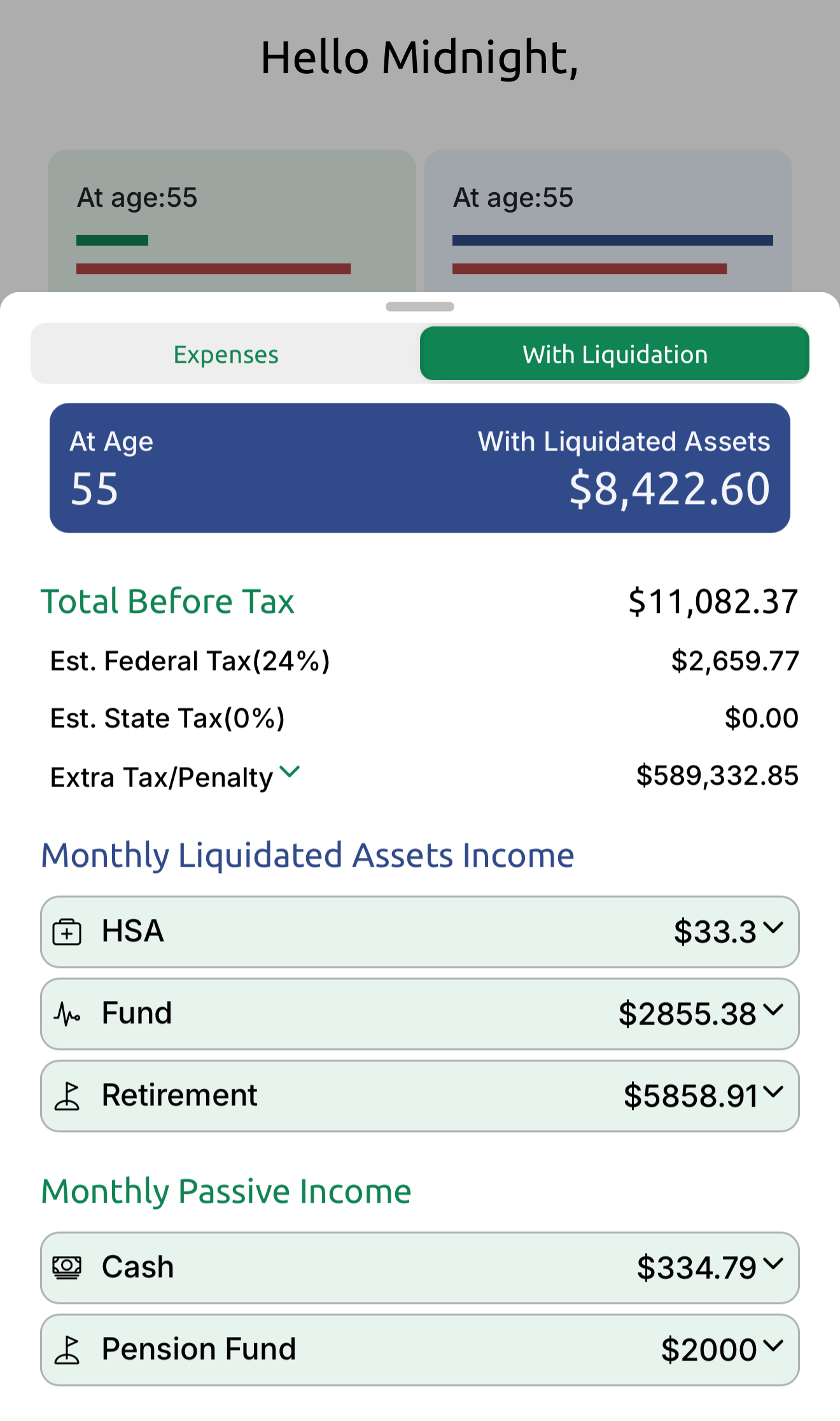

nnnnAs the focus is on asset liquidation and F.I.R.E. is achievable three years earlier than planned, it will be helpful to understand how these numbers are estimated. Tapping the top tiles gives that analysis. In this case, tapping the blue tile opens up the details

nnnn

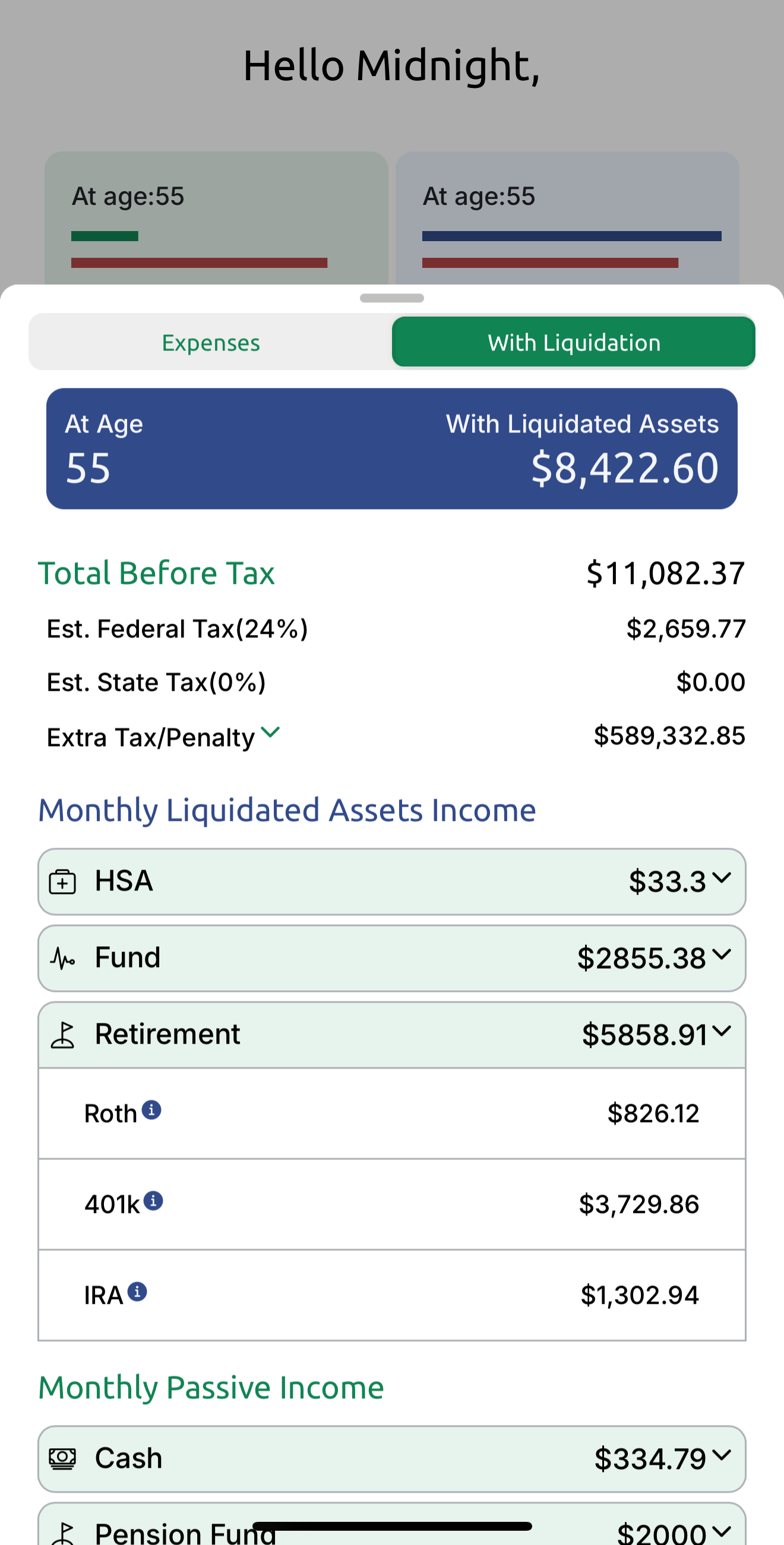

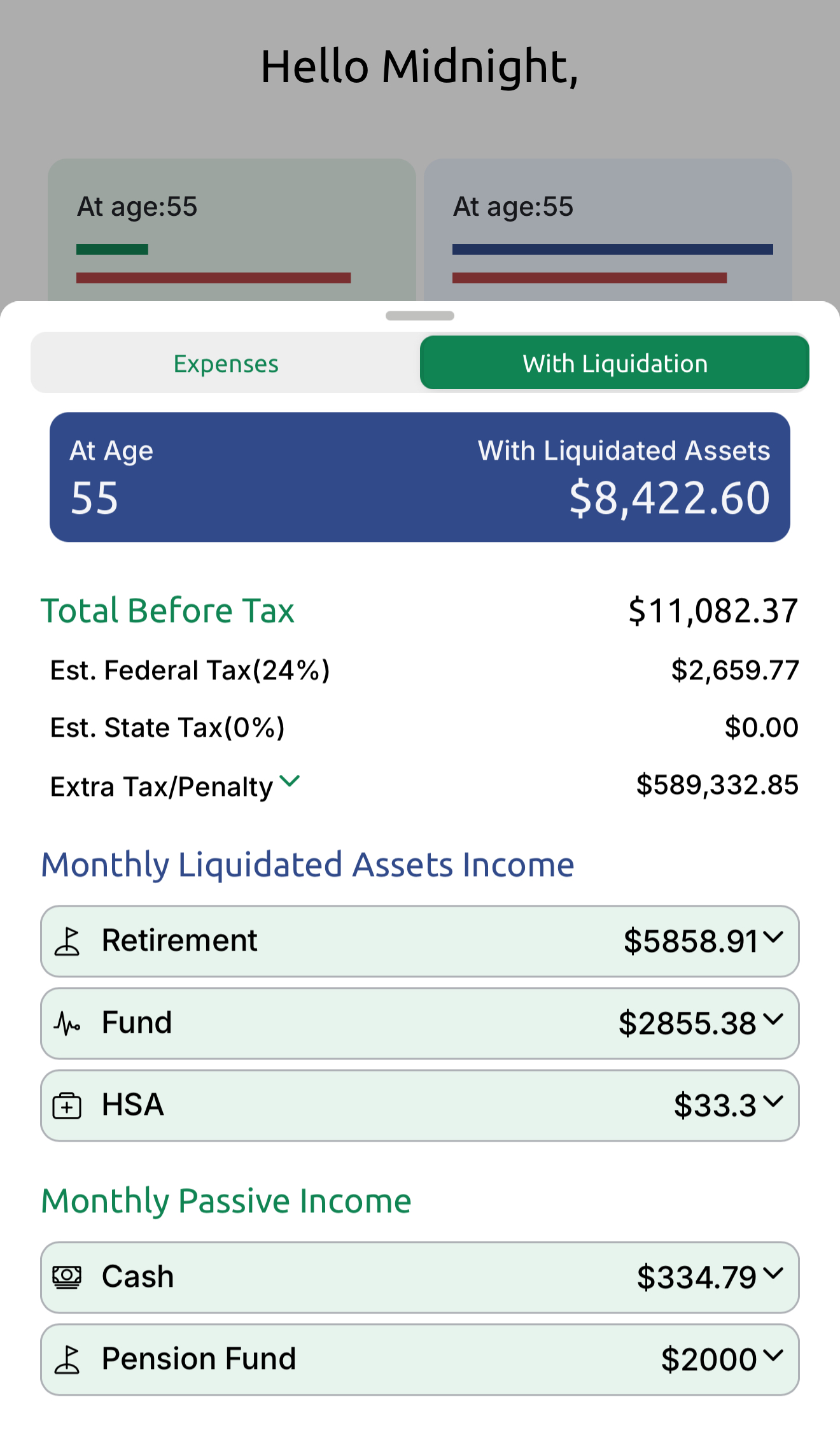

You will notice a lot of data in this screen. The top part shows that at age 55, the monthly passive income would be $8,422.60 by liquidating assets and reinvesting those at an assumed rate of return of 5%.

nnnn

The section below shows the total amount of $11,082.37 before estimated federal taxes of $2,659.77. There are no state taxes as the user is based in Texas. There is an "Extra Tax/Penalty" which we will get to later.

The following illustrates the passive income generated by liquidating assets, including HSA, Funds, and Retirement accounts like IRA and 401K, as well as cash in HSA and the expected pension at age 55.

These sections can be further expanded to provide a detailed breakdown and explanation of the calculations. Clicking these sections would look like below:

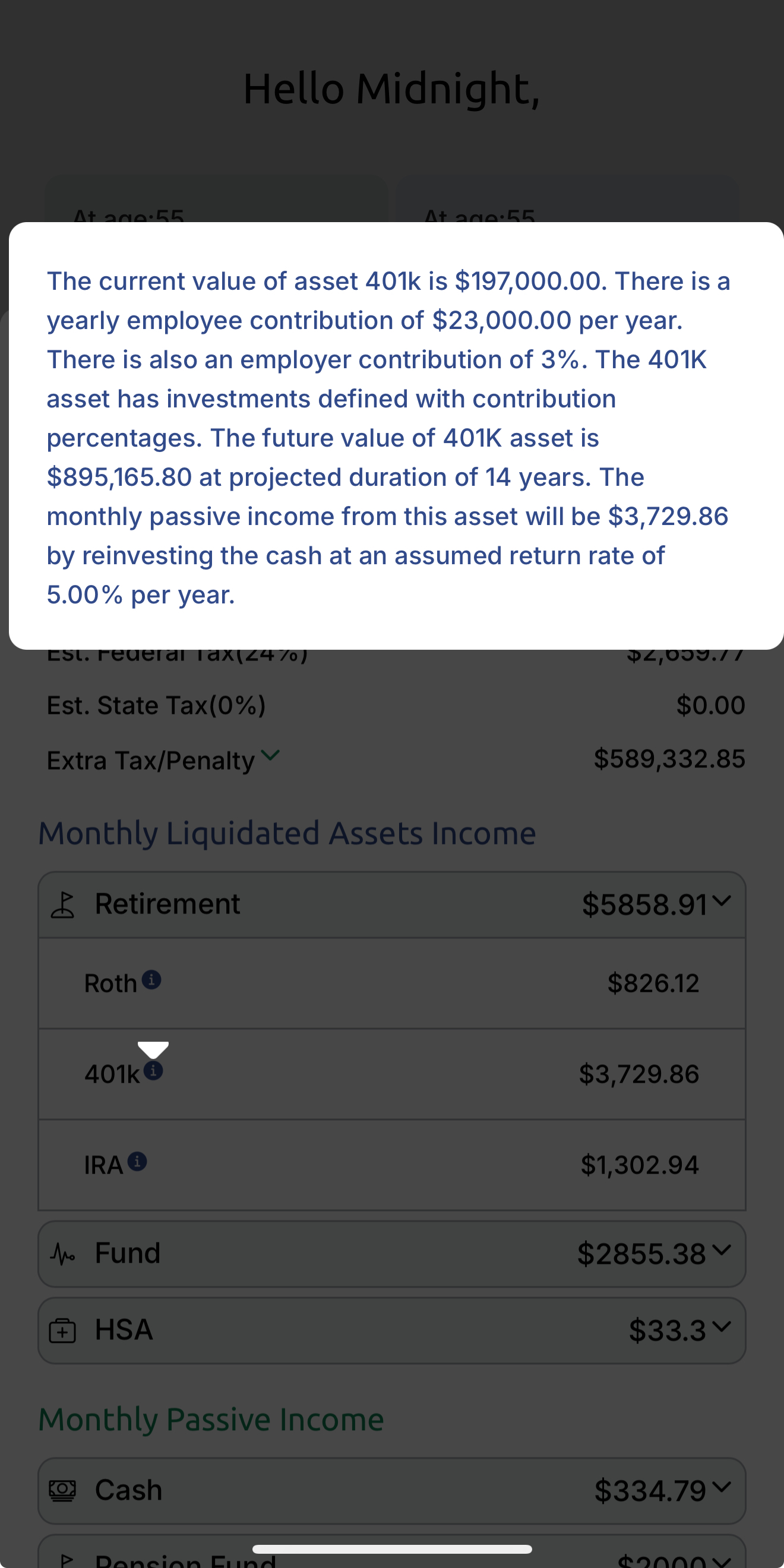

The first screen above shows the expanded "Retirement" section with passive income generated from each type of account. Tapping on each of these items shows an explanation of how those values are calculated. For example, the second screen illustrates how liquidating a "401K" account at age 55 can generate $3,729.86 in monthly passive income after reinvestment at 5%.

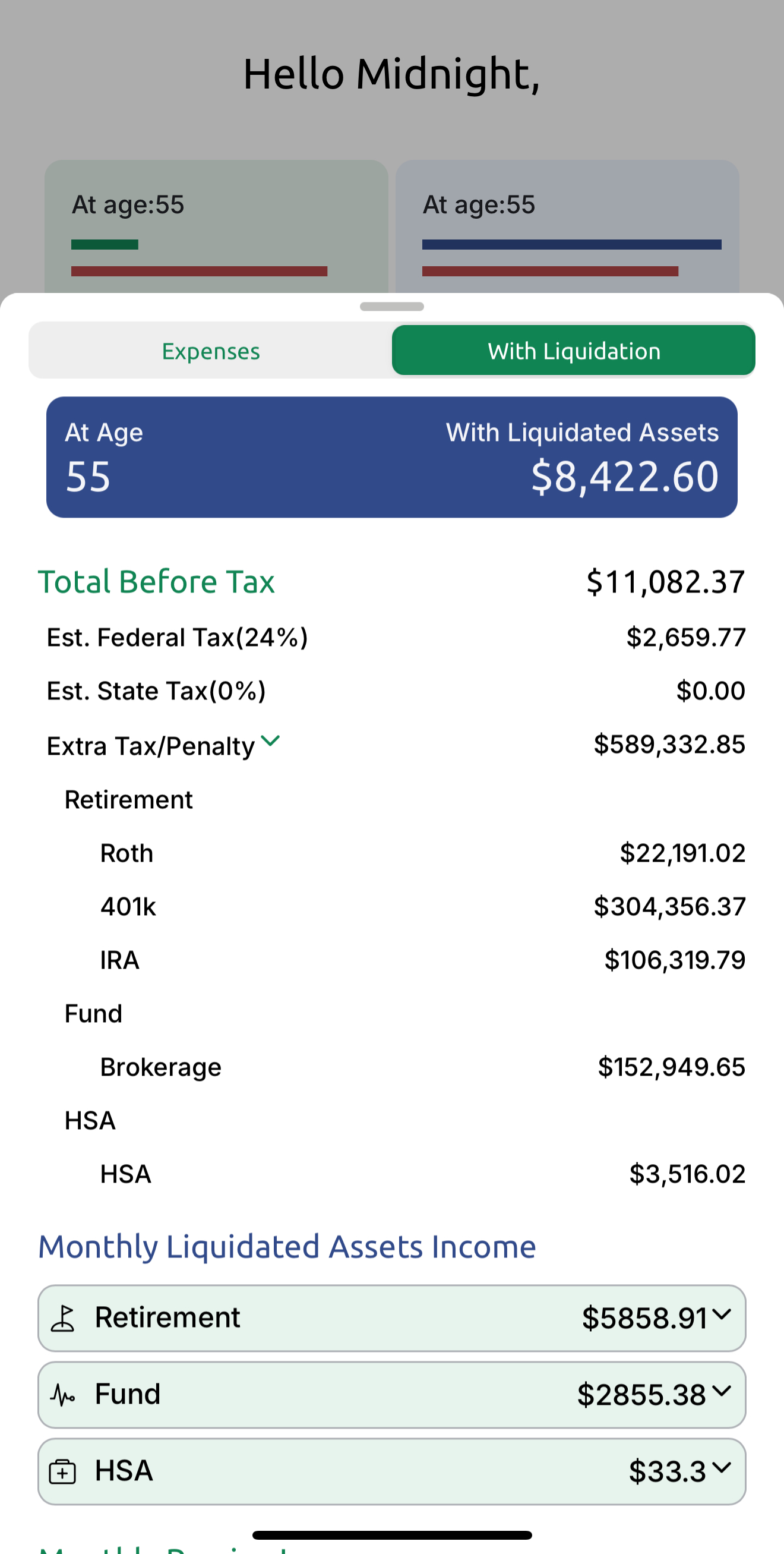

nnnnExtra Taxes & Penalties

nnnnLiquidating assets can have one-time severe impacts on applicable taxes due to capital gains and penalties due to early withdrawal from retirement accounts, such as 401K and other pre-tax contribution accounts, such as HSA for non-medical reasons. The screen below shows the total extra taxes and penalties, and a detailed breakdown. There will be an estimated $589,332.85 of applicable tax and penalties as a result of asset liquidation. This is separate from taxes on income from passive investments, as it is a one-time event.

nnnn

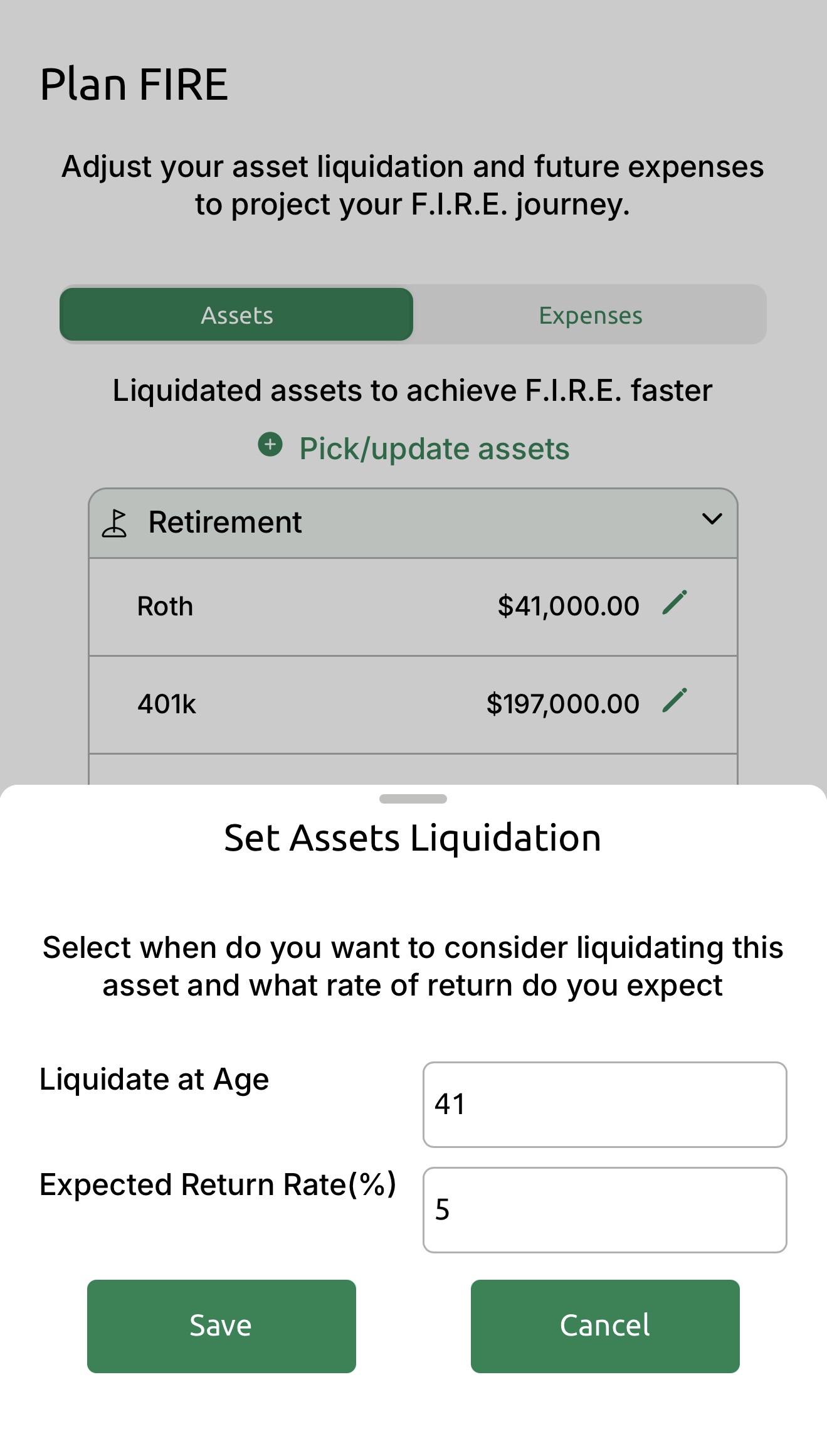

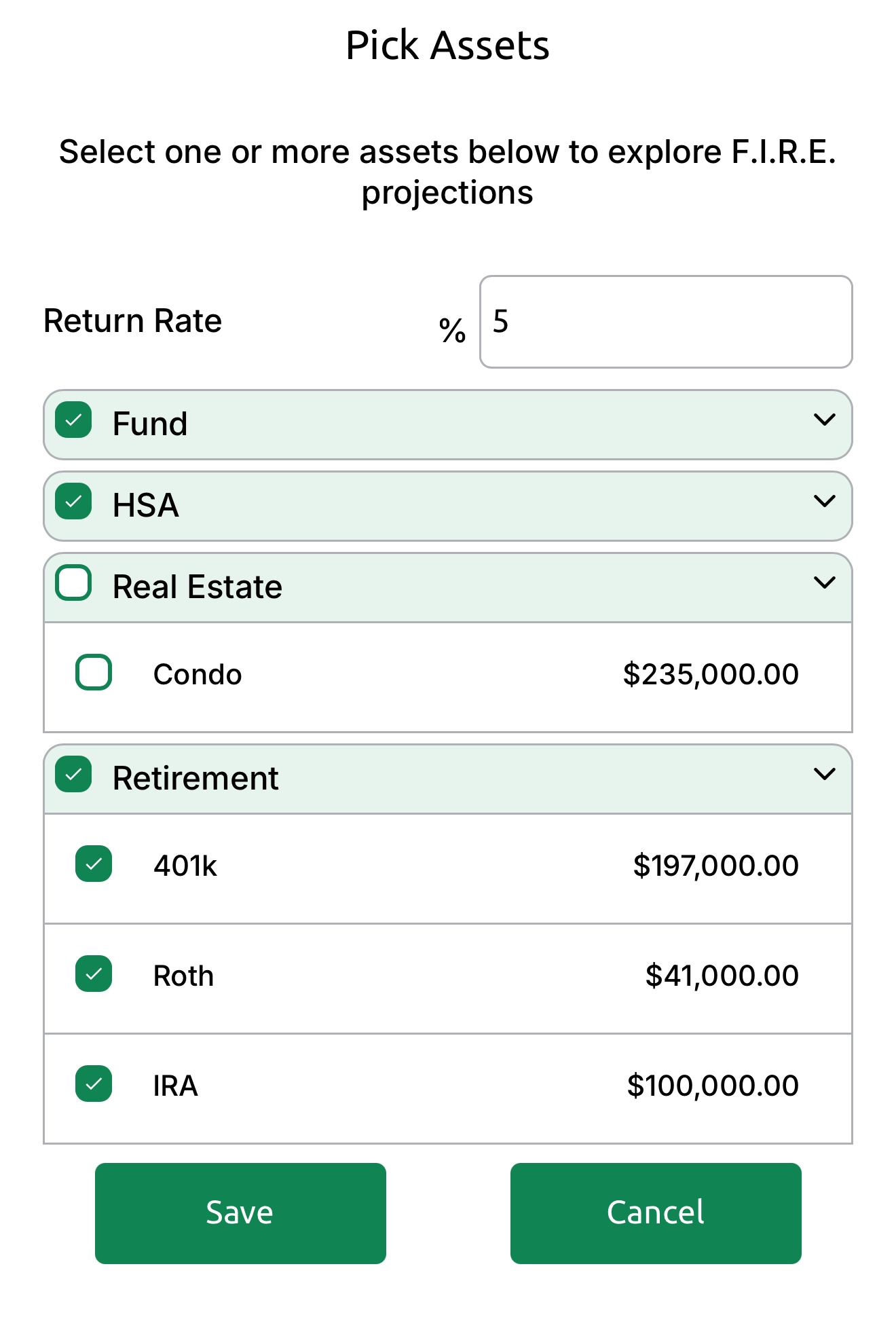

Fine Tuning

nnnnIt is very common not to liquidate all the assets at retirement. As an example, this user wanted to retain their condo rather than liquidate it. To do this, go to the "Plan F.I.R.E." option on the home screen and adjust preferences, such as excluding certain assets, updating the rate of return, or selecting a different age to liquidate. It looks like this:

nnnn

The first screen displays selected assets to liquidate, along with an option to choose a different age for liquidation and an expected rate of return for reinvestment. The second screen displays options to exclude specific assets from liquidation; in this instance, the real estate asset 'Condo' is excluded.

nnnnClosing Remarks

nnnnThis system provides a detailed analysis based on various milestones, eliminating the guesswork. It provides the necessary confidence and offers a thorough analysis of the F.I.R.E. journey, including options for the passive-only path versus selectively liquidating assets. It is also possible to project future expenses. The system also considers the average inflation to bring these projections closer to reality.

nnnnn