Can You FIRE by 55 While Funding Kids Education?

This is an interesting use case where a FIRE enthusiast was wondering if he could still FIRE by 55 while hoping to fund his kids' education expenses of about $500,000. Here is the reddit post

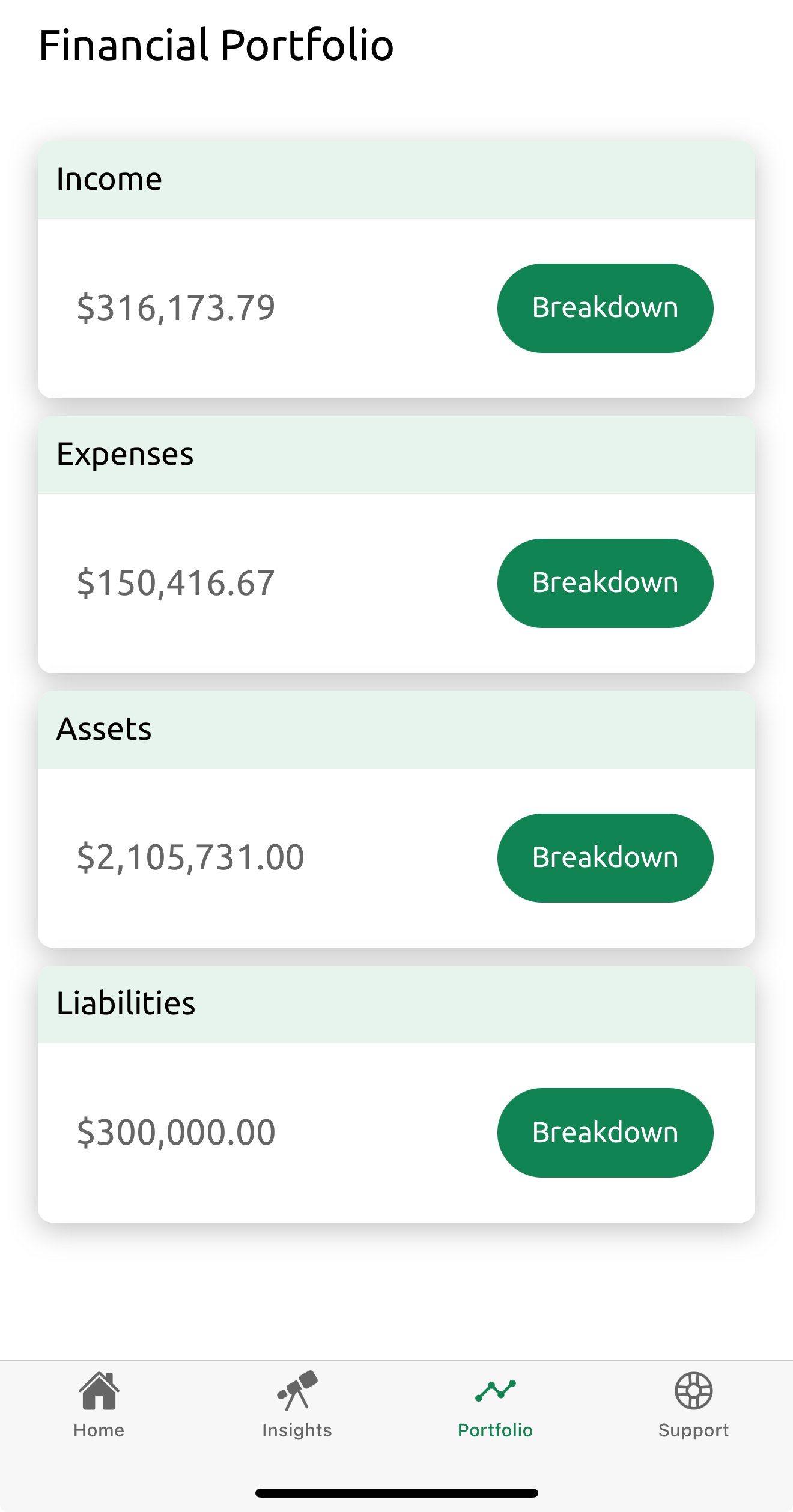

nnnnnnnnn46M in HCOL with two kids and spouse. NW ~1.8M. Household income is 450K, and expenses are 150K, including mortgage payments. 1M invested equally in a few growth stocks and growth ETFs (VGT, VOO). 750K in retirement accounts (30% Roth). 80K in cash reserves. (800K in home equity with 15 more years of payment left). Plan to fund kids' undergrad, so expecting 500K expenses in 6~10 years.

n

Please refer to the Reddit post for clarification on the situation to better model it in the Baniya App. So, the data modeling is relatively simple and can be done with the above data, and would look like below:

nnnn

This data is sufficient to get future projections using just passive income or by considering asset liquidation. However, the tricky part comes up on how to understand if it is possible to FIRE even after spending a one-time half a million for funding kids' education in a future year. Please note that a few assumptions have been made to explain this powerful feature. Two such assumptions are: only one kid is assumed for the entire $500,000, and it is averaged out to 8 years rather than 6-10 years (So the user will have this expense at the age of 54 years).

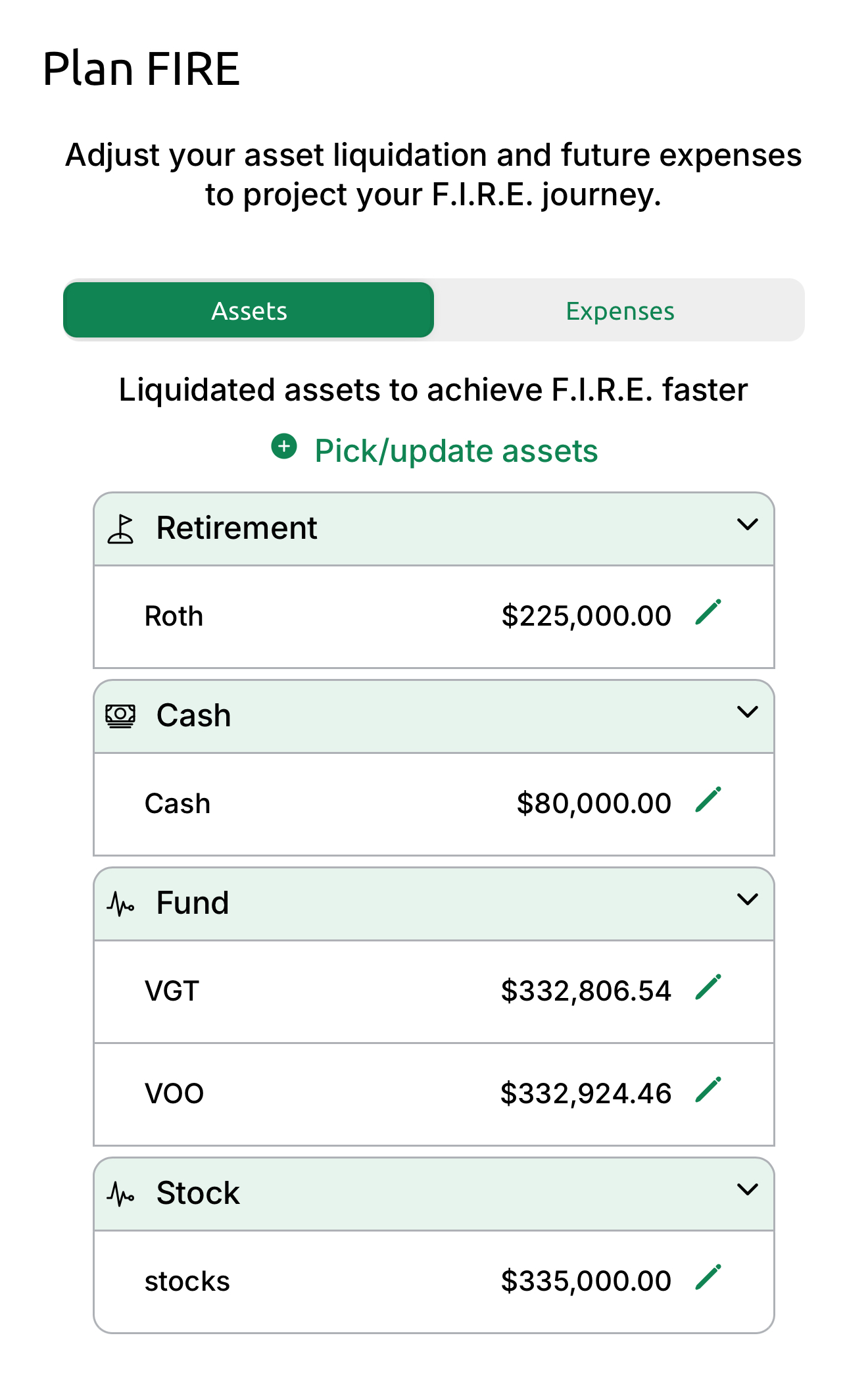

nnnnThe "Plan FIRE" option from the home screen allows two options:

nnnn- n

- Be able to opt out of which assets should not be considered for liquidation. In this case, the user never wanted to liquidate their home. nnnn

- Be able to add one-time future expenses. In this case, a $500,000 expense is considered at the age of 54. n

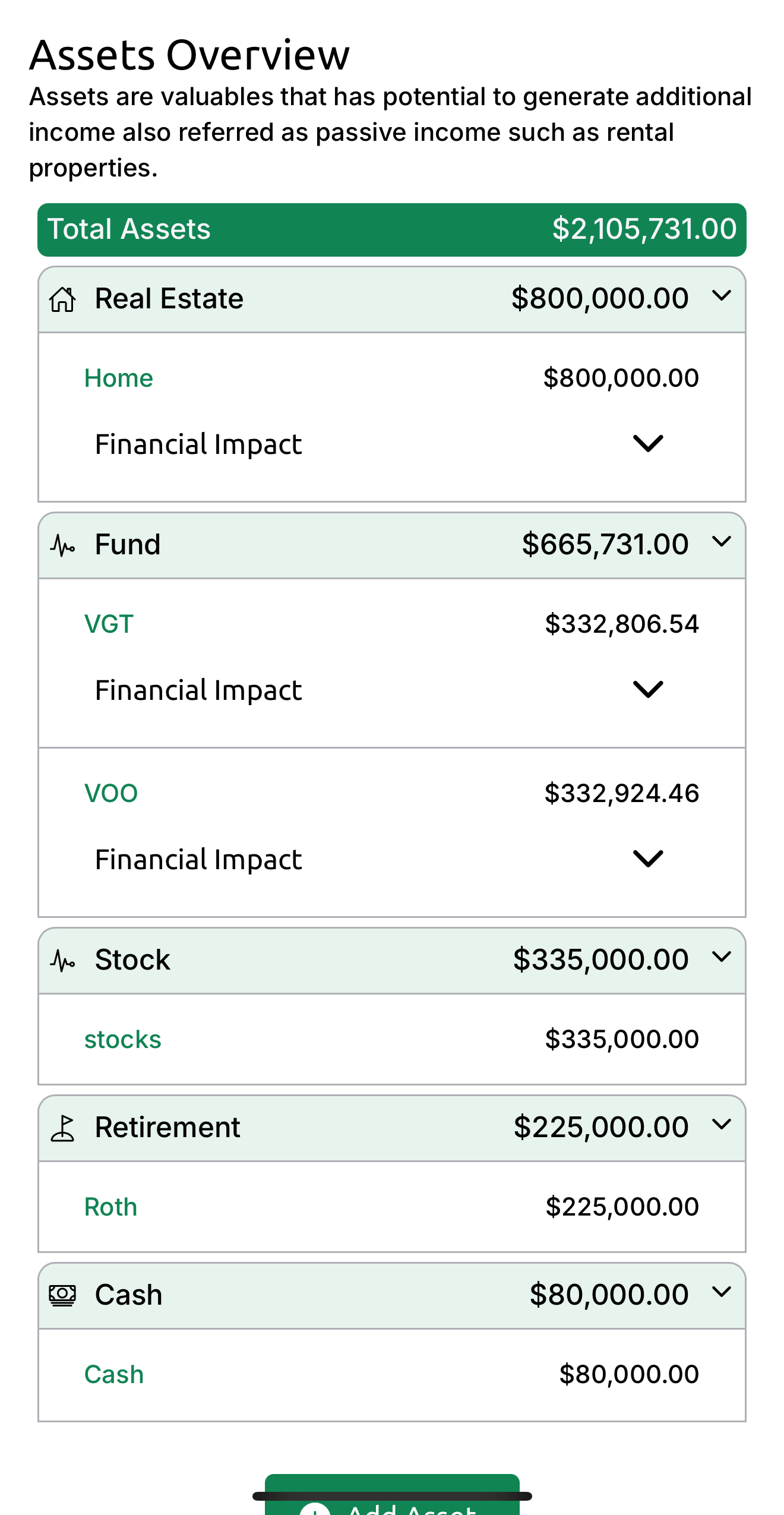

Below is how "assets" selection appears in the "Plan FIRE" area. You will notice that real estate is excluded from this list to prevent consideration for liquidation.

nnnn

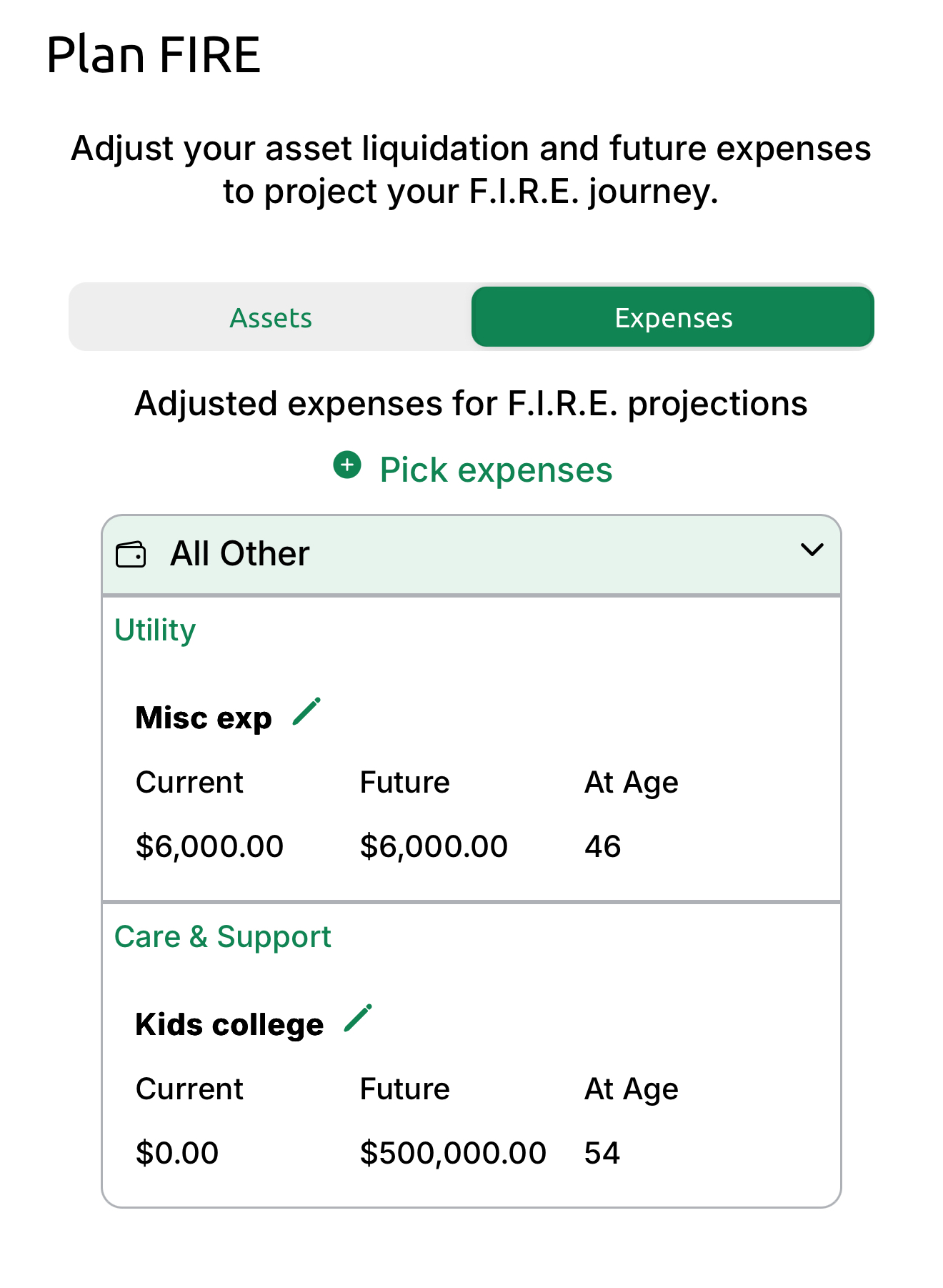

Below is what expenses look like after adding a one-time future expense of $500,000 at the age of 54.

nnnn

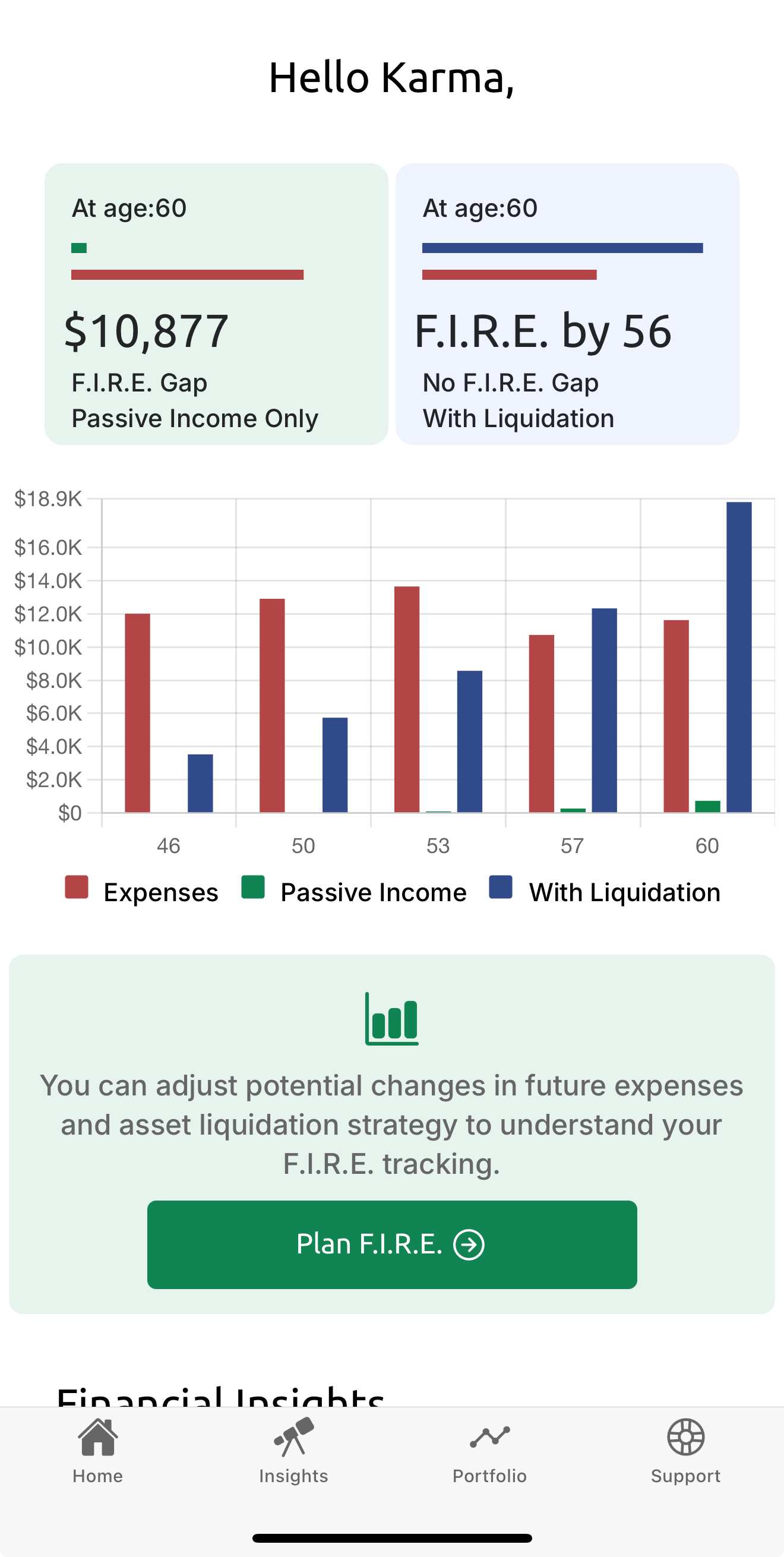

That's all it requires to finish the data modeling and this one-time expense adjustment. Going to the home screen shows the magic numbers and indicates the possibility of FIRE by age 56. Of course, the user would like to understand how this worked out and its impact. So, tapping on the blue box at the closest number, which is 57 in this case, shows additional details:

nnnn

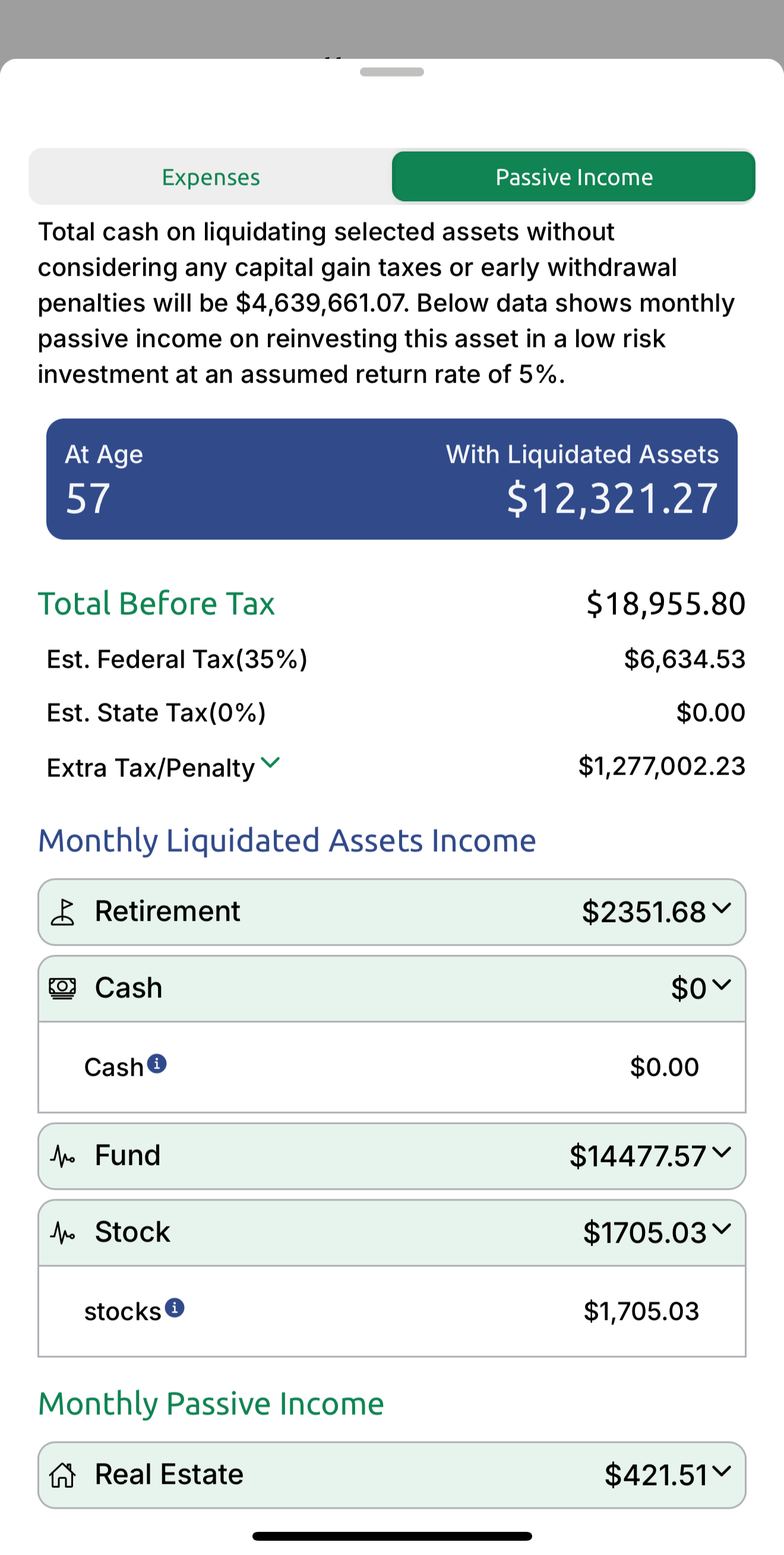

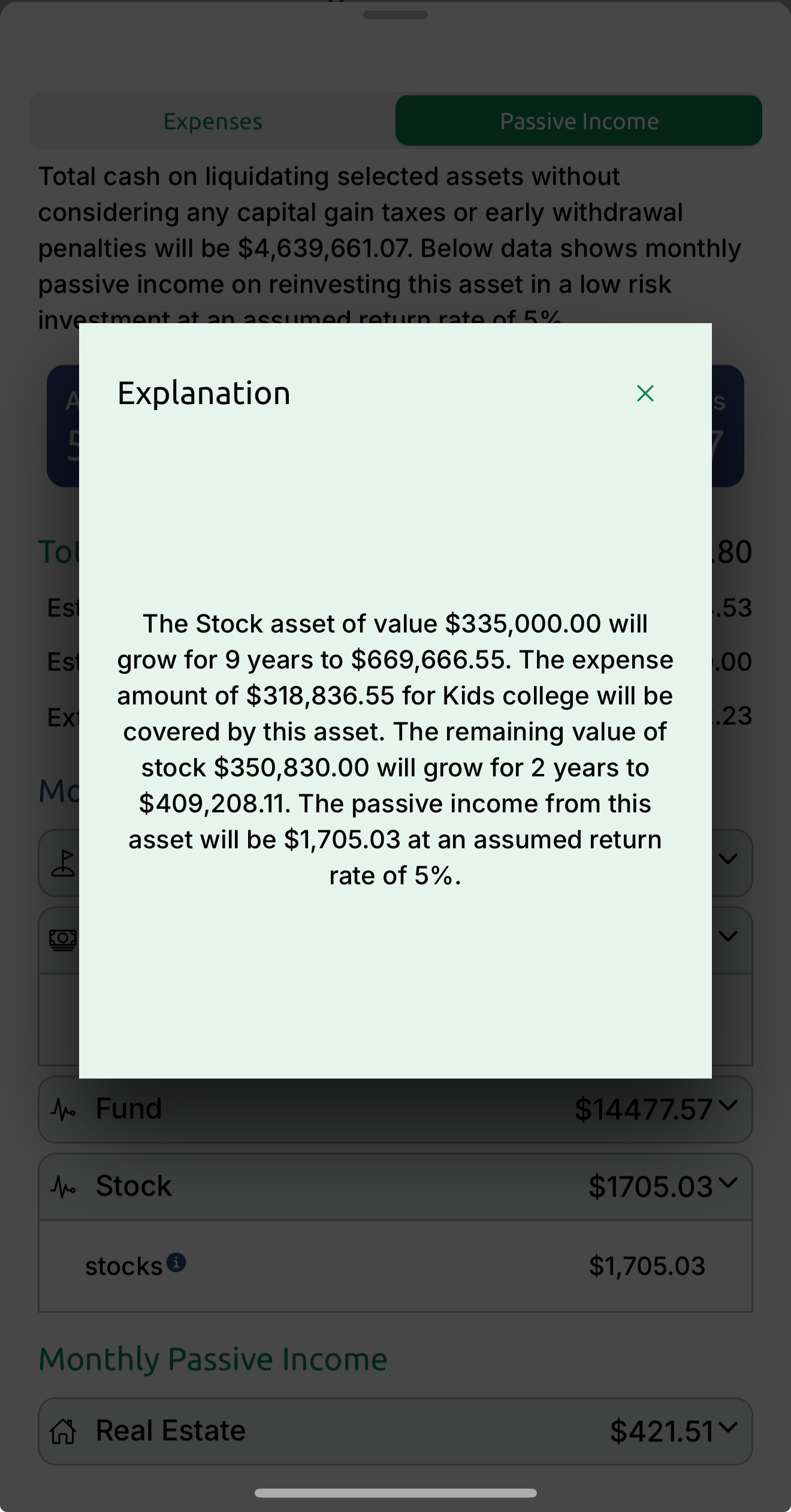

Looking into the details screenshot, you will notice that the "Cash" value shows $0, and you will also see the "stocks" asset. The little blue icon next to these shows a complete explanation of how these numbers are calculated, accommodating adjustments made by the user.

nnnn

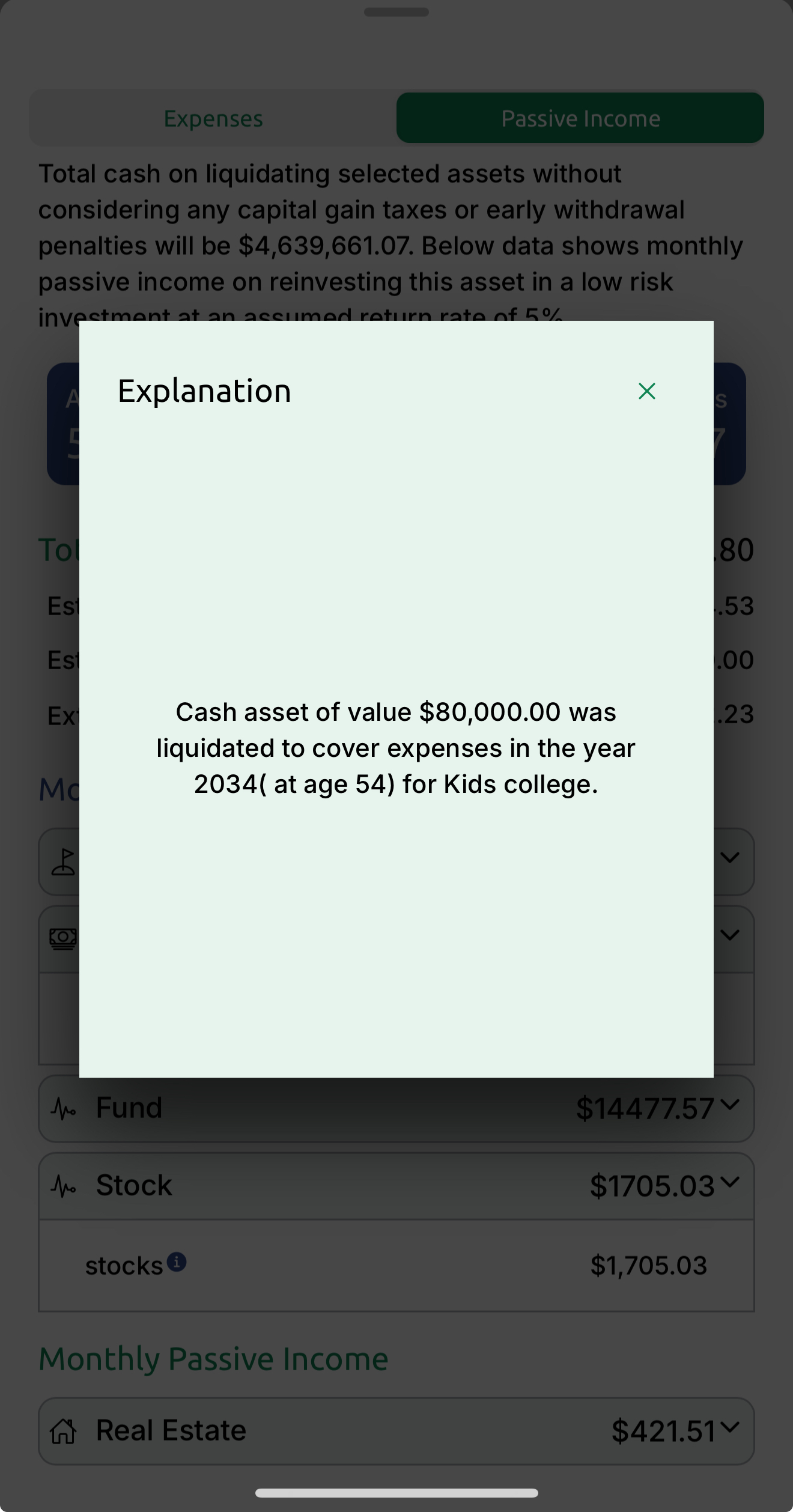

Tapping the cash asset, as shown in the first screen, explains why it is zero, as it was used to pay part of the kids' education at 54. Tapping the second screen shows that the remaining balance was paid by liquidating a portion of stocks. This did affect the growth of the stock portfolio, but it still managed to grow with the remaining stocks. If you are curious about why stocks were chosen for liquidation over funds, the reason is that stocks have a lower return rate based on the provided data compared to funds.

n